Since launching two months ago, Chainflip Lending has already attracted $1.47M in total TVL, with over 400k in active loans. Lending 2.0 builds on that early traction by unlocking more utility from the capital already supplied to the protocol.

With this upgrade, supply across all assets can be used as collateral. For BTC specifically, this also unlocks additional yield through Boost.

The goal is simple: make lending more useful for LPs, help them use capital stored in the system more efficiently, unlock new protocol fee sources, and attract more users to Chainflip as a whole.

Here’s what’s changing, what it means for your existing position, and why we’ve built it this way.

What's Changing

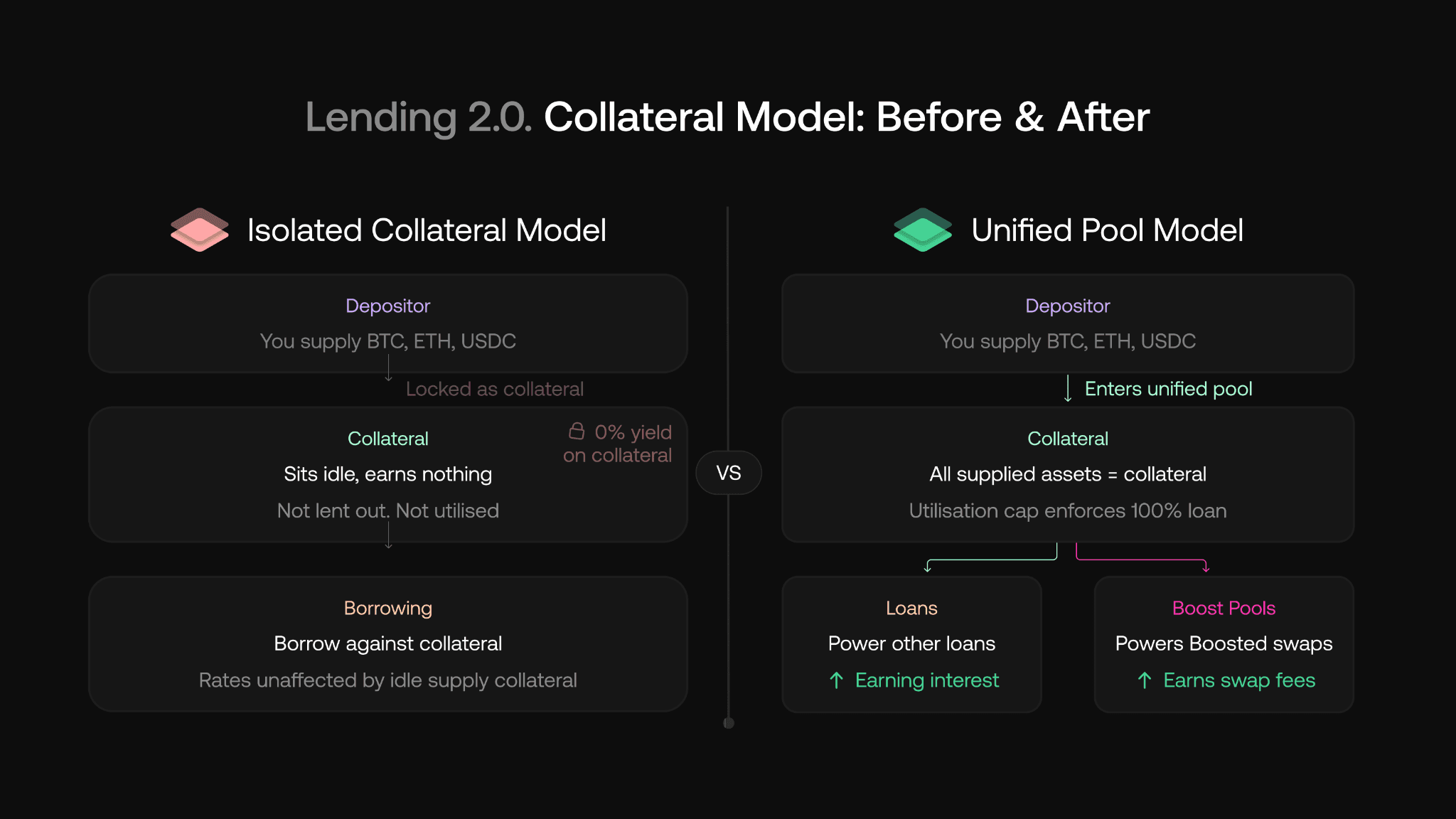

Right now, Chainflip Lending uses a simple collateral model: you supply collateral to borrow, but that collateral is not able to be lent out, and its underlying value remains unutilised.

With Lending 2.0, we're moving to a unified pool model where all supplied assets become collateral, in a similar fashion to the default settings of existing DeFi lending protocols. This will mean that supplied collateral can be used in other loans to offset the cost of borrowing, making the lending product as a whole more attractive for both passive suppliers and borrowers. This is paired with limits that ensure we have full loan coverage when issuing new loans.You can read more about how the lending mechanics work in our lending documentation.

As part of this change, the auto-topup feature will be removed. Instead, lending positions will rely on the updated collateral model and loan coverage limits introduced with Lending 2.0.

The yield benefit is especially exciting for BTC. Boost is a perfect fit for yield-earning collateral because it can generate an attractive APY even at very low utilization. This means BTC suppliers and borrowers can still benefit from Boost yield, even while Lending 2.0 maintains full loan coverage.

Because Boost only operates on Bitcoin, BTC supply in the unified pool will be partially utilized to power Boosted swaps and deposits. This helps offset the cost of borrowing and makes BTC-backed loans, as well as passive BTC supply, far more attractive to market participants not already engaged in the Chainflip ecosystem. If you're new to how Boost works, our piece on earning BTC yield with no impermanent loss is a good starting point.

Legacy Boost pools are staying. Boost is Chainflip’s Bitcoin liquidity product, allowing LPs to speed up BTC swaps by providing Bitcoin liquidity before normal confirmation times have passed. Since launch, Boost has earned over $440,000 in fees and sped up more than $1.27B in trading volume.

If you want to supply BTC purely for Boost without lending exposure, you can still do that through the existing Boost pools. But if you have a BTC lending position, you’ll now be able to earn Boost yield on top of your lending position.

For current lenders, this one is important.

All existing loans across all assets will migrate to the Lending 2.0 model automatically. You don't need to do anything to trigger this, but you should understand what changes for your position.

Previously your collateral was locked and earning nothing. From the Lending 2.0 launch, your supplied collateral will be deployed into the unified pool and begin earning interest from any loans taken out against it in that unified pool. If you are uncomfortable with your collateral being used in other loans, you are welcome to withdraw your position via the lending app.

Supply as Collateral: Utilisation Caps Protect Liquidation Capacity

Supply as collateral may initially sound like it adds risk to the lending protocol, but that risk is managed. Lending 2.0 enforces a utilisation cap on every asset. A new loan is rejected if it would reduce loan coverage below 100%.

This ensures there is always enough of each collateral asset available, meaning not locked in outstanding loans, to fully liquidate all loans at current Oracle prices.

Actual utilisation can still temporarily exceed the cap due to price movement or supplier withdrawals, but no new borrowing will be allowed until the pool recovers. The cap exists specifically to stop a large boost deposit or, in the future, a liquidity lending transaction from leaving BTC unavailable for liquidations. Boost will now draw liquidity from the lending pool, so the cap protects the lending system from Boost-driven liquidity spikes, as well as any other borrower activity that may drive shortages or loan collateral.

Having 100% loan coverage is a very conservative default setting, as there are almost no scenarios in which 100% of loans will need to be liquidated at the same time (other than in asset pools with a small number of loans). Partial liquidations, such as those that exist within the Chainflip Lending system, can get loans back to healthy LTV levels without requiring full liquidations. Even in extreme market drop scenarios, a 30% devaluation in BTC in a 24-hour period would not trigger many liquidations in a lending market where the global LTV is at 50-65%, which are quite typical levels seen in the industry.

Treating supply as collateral allows for much greater market efficiency and increases the attractiveness of the Chainflip lending product through natural rate improvements. Unlike many other DeFi lending markets, the number of assets we support is limited to a handful of native-only, non-hybrid asset pairs, limiting the inherent risks with lending products that have afflicted DeFi protocols of late, creating an incentive-free but still attractive lending market for borrowers and lenders alike.

Leveraging Lending to Improve Boost Liquidity & Generate a Competitive Edge for Chainflip Lending

As a further change, Boost liquidity will now be drawn from both legacy Boost pools and partially from the BTC supply in the lending protocol where available.

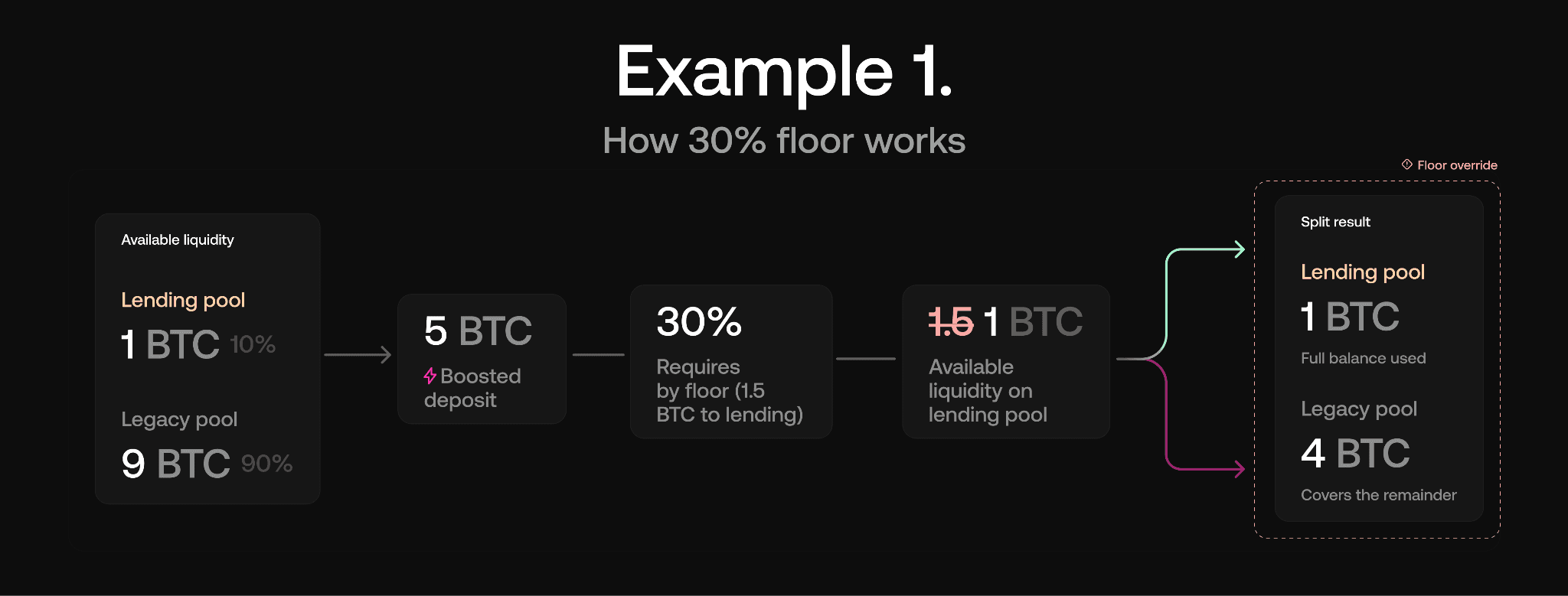

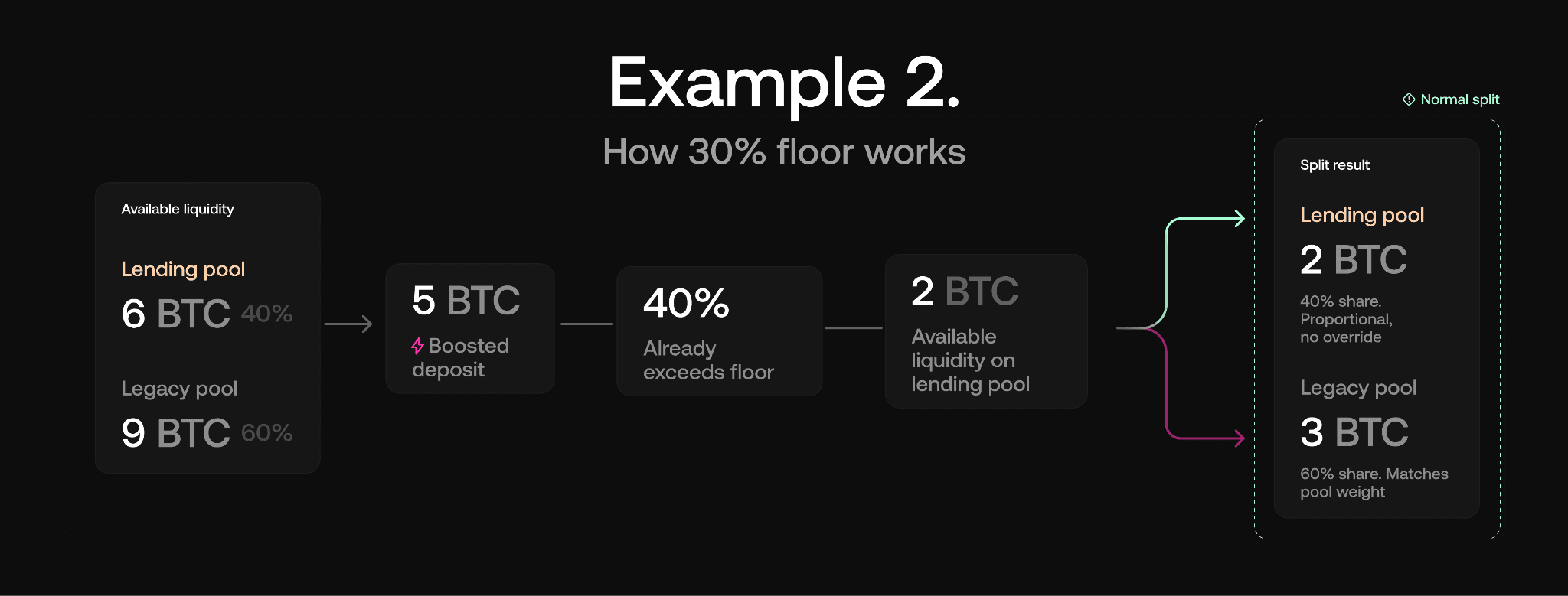

This is done proportionally based on available liquidity, with a floor of 30% coming from the lending pool when it has sufficient funds. This ensures that some Boost fees are directed towards the lending pools to incentivise BTC supplying and borrowing against it, while still ensuring a strong yield for legacy pool users to maintain liquidity in that pool.

Example 1: Legacy has 9 BTC available; the lending pool has 1 BTC. A 5 BTC deposit comes in. A proportional split would give the lending pool 0.5 BTC, but the 30% floor guarantees 1.5 BTC. The lending pool only has 1 BTC, so it provides 1 BTC, and legacy covers the remaining 4 BTC.

Example 2. Legacy has 9 BTC; the lending pool has 6 BTC. A 5 BTC deposit comes in. The lending pool holds 40% of total liquidity, which is already above the 30% floor. Lending provides 2 BTC; legacy provides 3 BTC.

This keeps legacy Boost productive while providing benefits to new users who will bring BTC liquidity to the lending system.

Reorg risk now applies to BTC lending positions

Because BTC supply in the lending pool now powers Boosted swaps, BTC positions are exposed to chain reorg risk that previously only applied to standalone Boost depositors.

If a Bitcoin block is reorged and a Boosted swap is reversed, the protocol’s reorg protection mechanism may draw from the pool. This risk is not eliminated; it is shared more broadly across BTC participants in the lending system. Positions in other assets are not affected.

That said, this risk remains extremely low. Since Boost launched two years ago, Chainflip has lost zero deposits to Bitcoin reorgs.

Chainflip’s decentralised validator design also helps reduce the likelihood of dangerous Boost exposure. If the Bitcoin network experiences a partition, which is one of the more likely causes of a reorg, Chainflip validators are unlikely to agree on the same deposit quickly enough to pre-witness and Boost it. In that case, the protocol would wait for the normal full witness process instead.

While we did recently see a rare 2-block reorg on Bitcoin, no transactions were dropped in that reorg. A dangerous reorg that could meaningfully impact Boosted deposits remains extremely unlikely and would require a highly adversarial Bitcoin network event, such as a 51% attack.

Low LTV penalisation rates

Lending 2.0 carries over the low LTV penalization rates from lending. If you're borrowing at a conservative LTV, you'll still be protected from liquidation, but your interest rate may reflect your lower collateral efficiency. These rates are worth being aware of:

1% APY at 0% LTV

0% APY at 50% LTV

If you want to optimize your rate, review your LTV and consider whether your current collateral level makes sense under the new model. For more on how LTV affects your position, see our guide to BTC-backed loan use cases.

What Happens to Legacy Boost Yields

Legacy Boost pools remain for now, but their yields will be affected by this change.

Under Lending 2.0, Boost draws liquidity from both pools proportionally with a 30% floor for lending. If you're currently in a legacy Boost pool and want to maintain yield on your BTC, migrating into the lending pool may be worth considering, but the risk appetite is yours to determine.

Early Depositors Have an Edge

Yields in the unified pool will be most attractive early, before the pool is deep with supply. As more deposits come in, fees are distributed across a larger base, and per-depositor returns normalize. If you have an existing loan, you're already in the pool from day one.

Making Lending More Attractive and Improving Overall Protocol Liquidity

The old model had a structural inefficiency: collateral was deposited but earned nothing, and Boost pools sat separately with no connection to lending supply. The unified model brings these together. All supplied assets become collateral, and for BTC, that supply also powers Boosted swaps and earns swap fees.

The tradeoff is a more interconnected model, with managed risks now more interrelated but still limited to the lending protocol itself. Utilization caps enforce 100% loan coverage when issuing new loans (be they Boost, Liquidity, or general loans). Boost draws from both pools proportionally rather than cannibalising one and risking a loss in total BTC boost liquidity should the BTC lending product fail to attract liquidity.

Summary

For existing loan holders:

All supplied collateral moves to the unified collateral model automatically

BTC supply positions specifically become yield-bearing via Boost fees

Review your LTV if you want to optimise your interest rate under the new model

For legacy Boost depositors:

Lending supply will now also count towards Boost pools for swap routing. For LPs and swappers, there will be no visible changes, other than an expected increase in Boost liquidity available.

Early BTC lending participants are expected to benefit from higher APY while lending-based Boost liquidity remains below 30% of legacy Boost liquidity. For existing Boost depositors, this creates a clear migration opportunity: move BTC into lending to continue earning Boost yield while also unlocking collateral utility.

For new depositors:

Supply BTC to the lending pool, use it as collateral to borrow, and earn Boost yield that can help offset your borrowing costs.

Legacy Boost remains available if you want pure Boost exposure without lending

Early supply earns higher yields before the pool matures

Resources

Swap Now - Start swapping native assets

Lend BTC - Borrow against native Bitcoin

Blog - Product updates and announcements

Chainflip Scan - Track swaps and network activity

Website - Explore Chainflip

Other Chainflip Products:

Boost - Earn fees by providing single-sided liquidity with no IL risk

Stablecoin Strategies - Deposit stablecoins and earn optimized yields

Provide Liquidity - Supply assets to Chainflip's liquidity pools

Stake FLIP - Delegate FLIP and earn staking rewards

Find us: