A month ago we shared the Lending 2.0 proposal. As of today, Lending 2.0 is live on lp.chainflip.io/lending.

Every existing loan and supplied balance has migrated automatically to the new model. If you already have a position, you do not have to do anything.

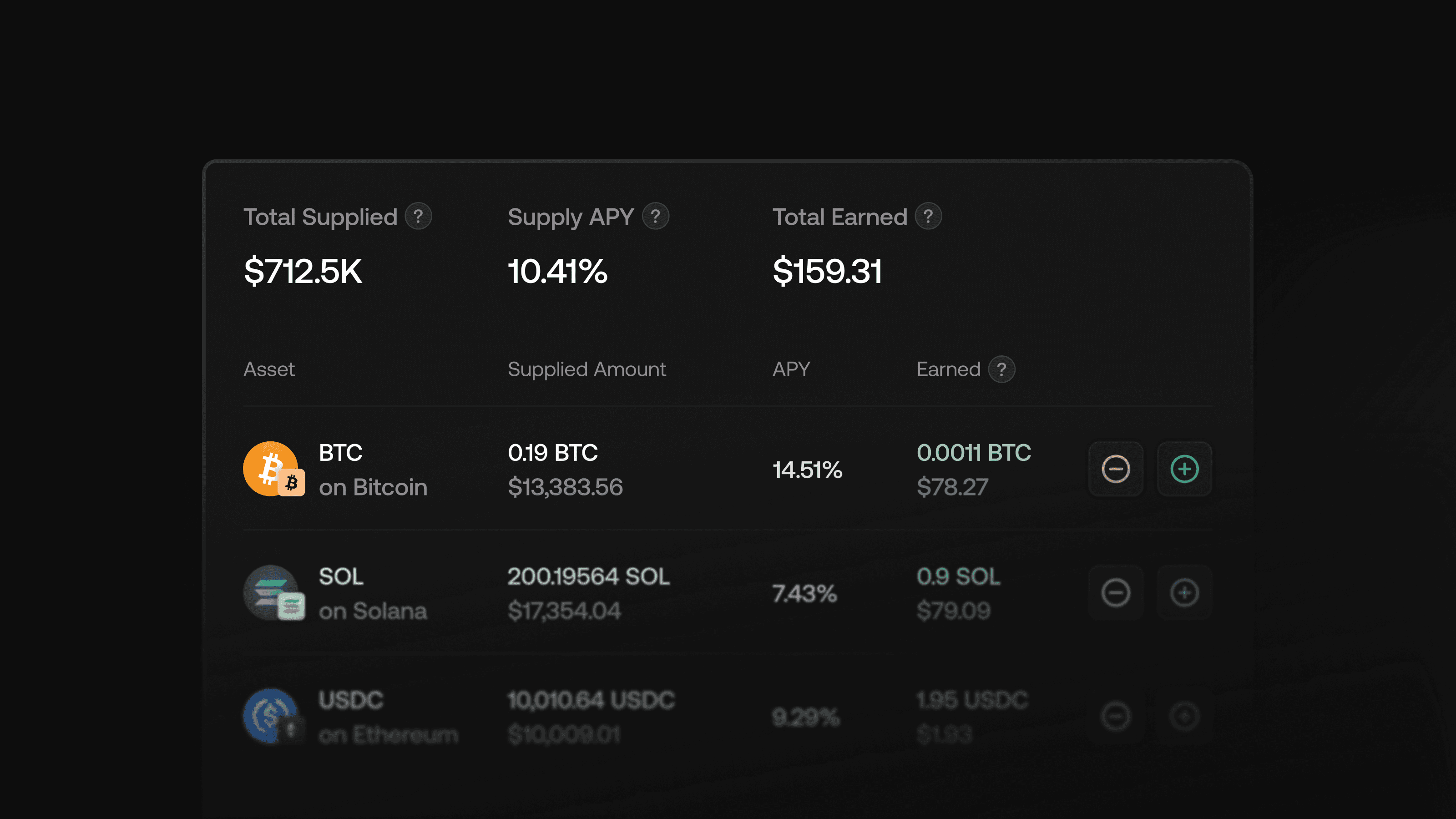

Where Lending stands today

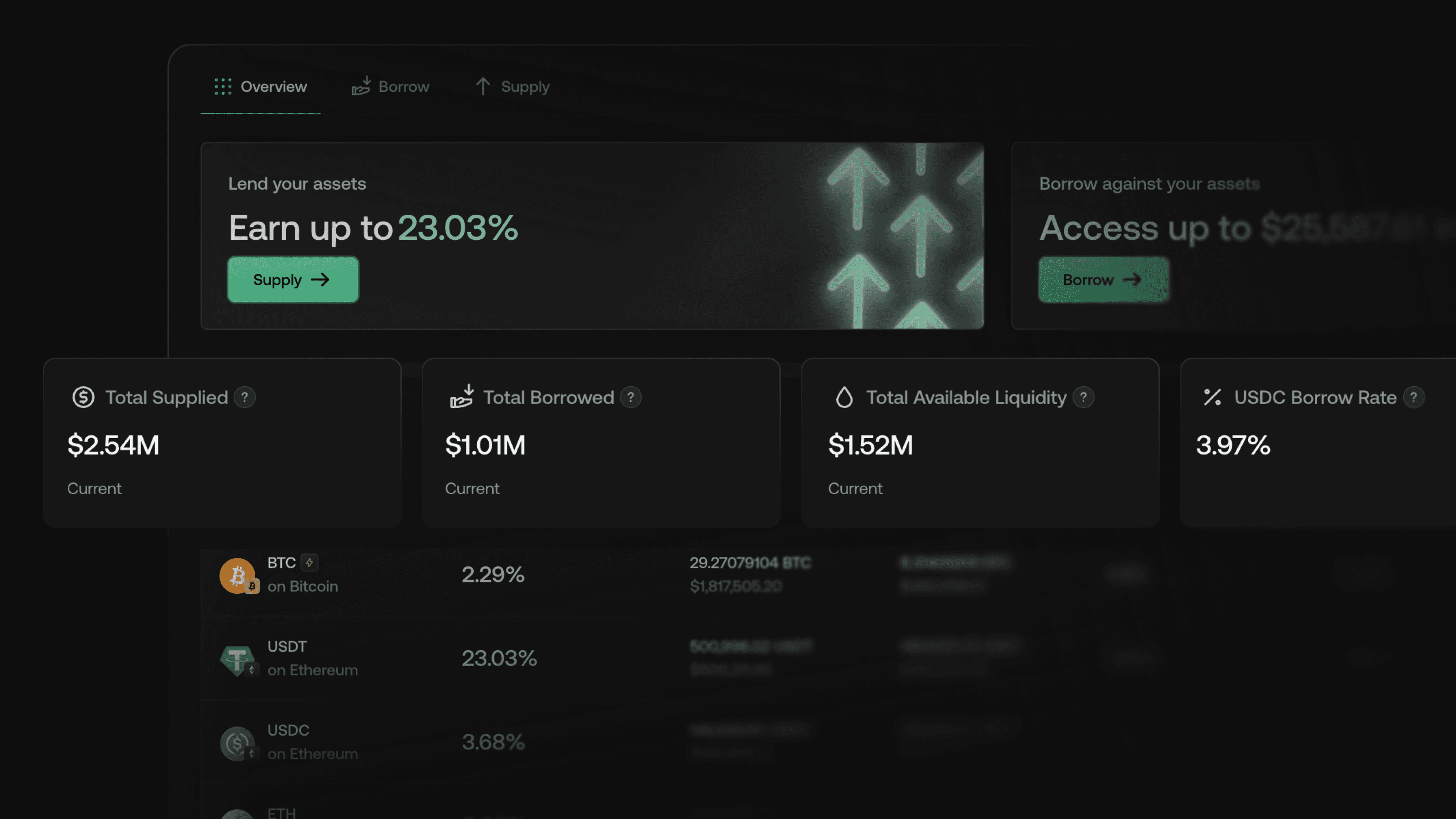

In the five months since the original lending product launched, it has grown to $2.5M TVL with $1M in active loans.

Lending 2.0 was designed to push that further by removing the dead-weight problem and pulling more BTC liquidity into productive use. Early depositors capture the highest yields. The pool will mature, rates will normalize, and the easy compounding window closes with it.

What Lending 2.0 changes for you

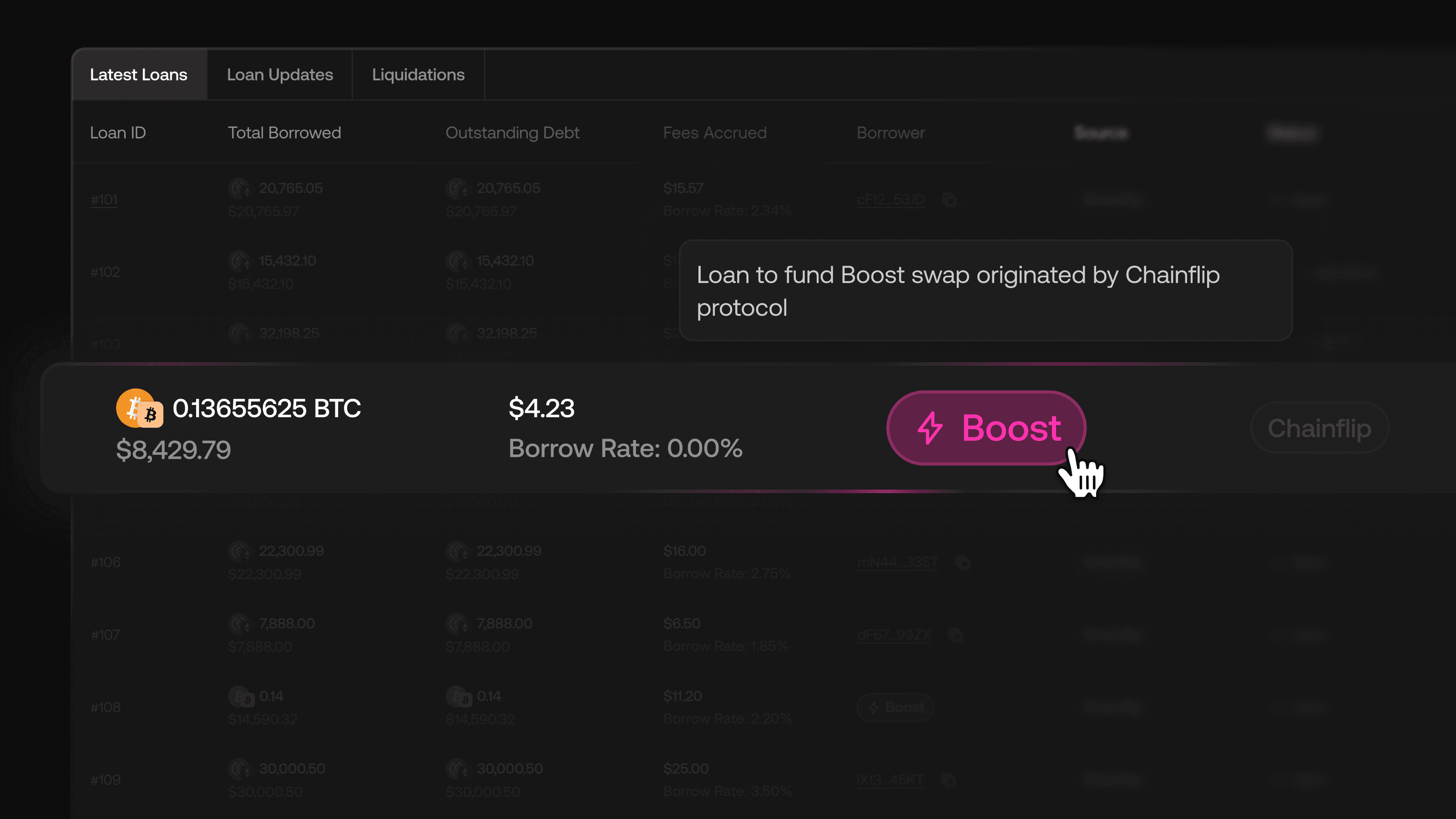

The original lending design treated collateral as dead weight. You would lock BTC, borrow USDC, and your BTC sat there earning nothing. Boost, Chainflip's 1-block finalisation BTC liquidity product, ran in its own silo. Boost and lending ran separately, so the two never worked together.

Lending 2.0 collapses that. The same BTC can back your loan and sit in the queue providing Boost liquidity. Your BTC now earns from two sources at once: lending interest and a share of Boost swap fees. Since Boost launched two years ago, it has earned LPs over $490,000 in fees while accelerating $1.5B in swap volume.

Until now, the only way to capture that yield was to commit liquidity to standalone Boost pools. Lending 2.0 opens that fee stream to anyone supplying BTC as collateral.

How it works

Supply enters a unified pool. Whether you are supplying BTC, ETH, SOL, USDC, or USDT, it goes into the same collateral pool that backs all loans.

BTC supply also routes through Boost. Boost liquidity is drawn proportionally from both legacy Boost pools and the unified pool, with the lending pool contributing at least 30%. BTC suppliers in Lending 2.0 earn a share of Boost swap fees on top of their lending yield.

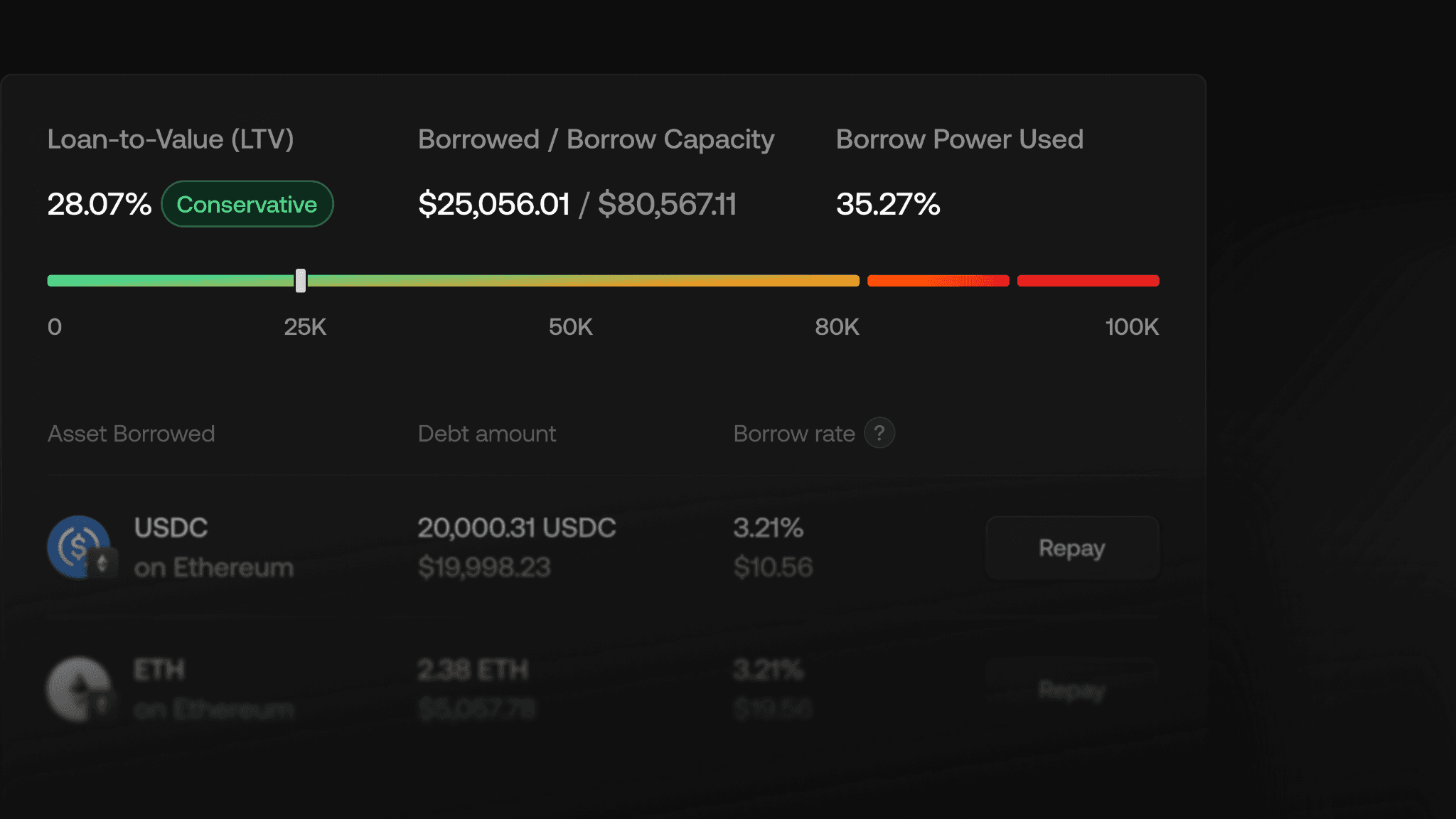

100% Loan Coverage is enforced. A new loan is rejected if it would drop coverage below 100%. That means there is always enough of each collateral asset on hand to fully liquidate every open loan at current oracle prices, we try our best to keep 100% coverage, but there are some caveats in practice.

Partial liquidations replace full unwinds. When an LTV gets risky, the protocol takes the smallest action needed to restore health, not the whole position. In practice 100% loan coverage is significantly more than what the system would need even in a big liquidation event.

What it means for borrowers

If you borrow on Lending 2.0, your supplied BTC does double duty. It backs your loan and, at the same time, earns a share of Boost swap fees. That Boost yield offsets the interest you pay, so the real cost of borrowing against BTC is lower than it would be in a standard lending market. For the first time, the collateral you post is productive rather than idle.

Borrowing is also more predictable. When a position gets risky, partial liquidations restore health by taking the smallest action needed rather than unwinding your whole position.

What it means for lenders

If you supply assets, it goes into a respective unified pool. Whether you supply BTC, ETH, SOL, USDC, or USDT, your supply earns interest whenever someone borrows against it, with no separate products to manage.

BTC suppliers get an extra layer. Your BTC also routes through Boost, so you earn a share of Boost swap fees on top of your lending interest, passively and with no opt-in required. As aforementioned, the early depositors capture the highest yields, since rates are most attractive before the pool matures.

What changed for existing users

All loans have already migrated. Your position is running on 2.0. Here are the main changes:

Auto-Topup has been removed. If you relied on it, review your LTV and top up manually as needed. Positions now rely on the updated collateral limits instead, which makes behaviour simpler and more predictable.

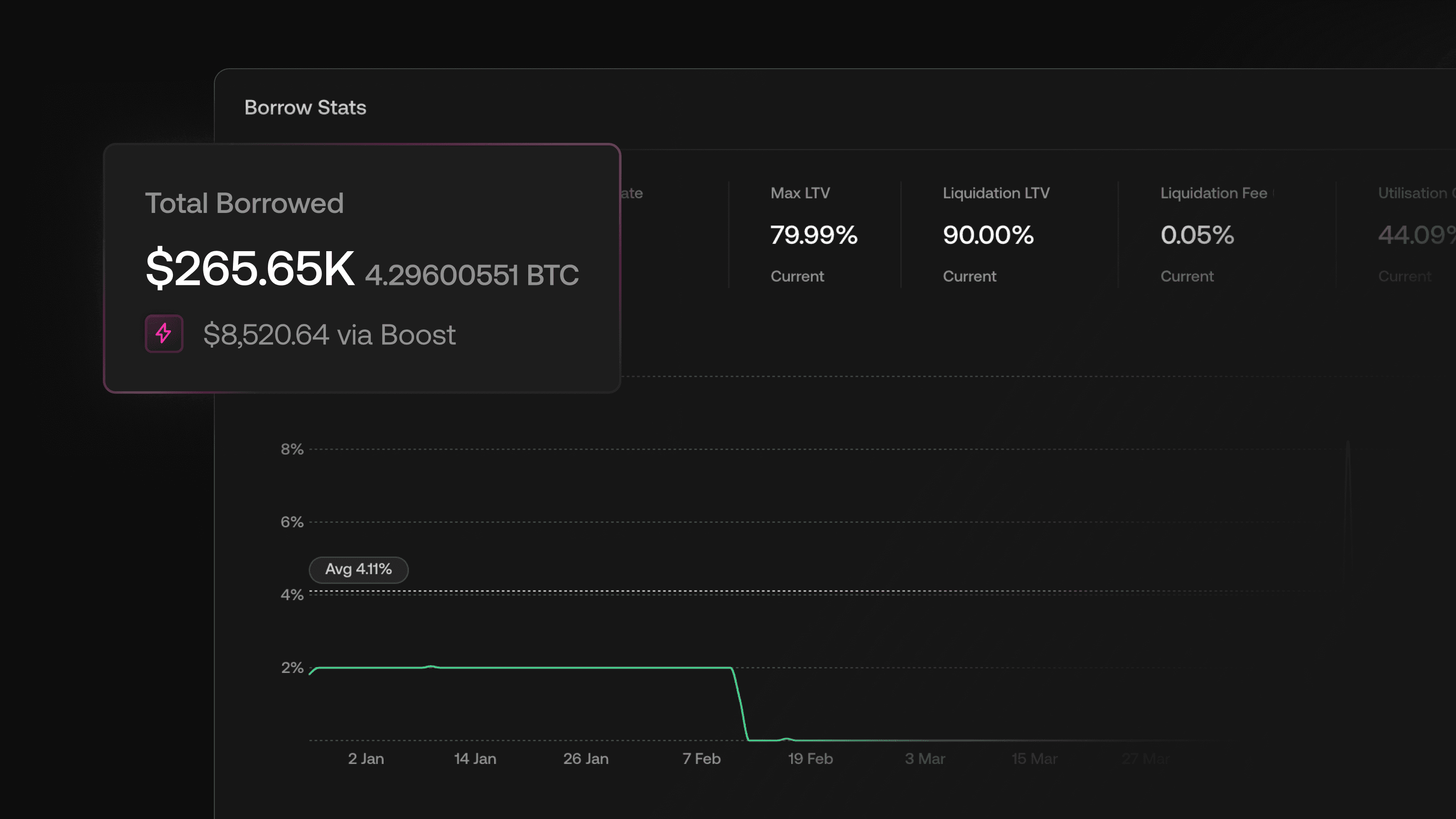

Your collateral now earns APY while it backs your loan, effectively lowering your real cost of borrowing. The interest curves have been adjusted accordingly: the utilisation junction is set to 50%, and the interest rate at that junction is set to 5%.

BTC suppliers are now earning Boost fees passively, with no opt-in required. Legacy Boost depositors are unaffected: standalone Boost pools continue to operate.

Legacy depositors can also migrate to Lending 2.0 to combine Boost fees and fees from regular BTC loans with collateral utility.

The risk you should know about

BTC suppliers in Lending 2.0 are exposed to Bitcoin reorg risk. It is the same risk that has always applied to standalone Boost depositors.

Since Boost launched two years ago, Chainflip has lost zero deposits to Bitcoin reorgs. That is the track record. It is not zero risk, but it is a track record worth weighing against the yield.

Try it

Lending 2.0 is live at lp.chainflip.io/lending. Supply BTC to earn from both lending interest and Boost fees, or borrow against your existing collateral.

FAQ

What changed in Lending 2.0? Every supplied asset is now collateral in a unified pool. BTC suppliers earn a share of Boost swap fees on top of lending interest, Auto-Topup has been removed, and the protocol enforces 100% Loan Coverage with partial liquidations. All existing loans migrated automatically.

How do I earn Boost yield on my BTC? Supply BTC into the lending pool. The protocol routes at least 30% of Boost liquidity from the lending pool, and BTC suppliers earn a proportional share of the Boost swap fees flowing through it. No opt-in required.

Do I need to do anything to migrate? No. All existing loans and supplied balances moved to Lending 2.0 automatically. One thing to know: Auto-Topup is no longer active, so if you relied on it, check your LTV and top up manually if needed.

What is 100% Loan Coverage? A rule that prevents a new loan from being issued if it would leave the protocol with less than enough of any collateral asset to fully liquidate all open loans at oracle prices. It is a tighter risk constraint than most lending markets enforce.

What is the reorg risk for BTC suppliers? BTC suppliers in Lending 2.0 face the same Bitcoin reorg exposure that has always applied to standalone Boost depositors. Chainflip has lost zero deposits to reorgs since Boost launched two years ago, but the risk is non-zero and worth understanding before supplying.