Borrow Against Bitcoin Instead of Selling: Lower Fees, No Tax Event, Full Upside

Borrow Against Bitcoin Instead of Selling: Lower Fees, No Tax Event, Full Upside

Borrow Against Bitcoin Instead of Selling: Lower Fees, No Tax Event, Full Upside

Selling BTC to access liquidity costs more than most people expect. The price on the screen is not what you receive. Capital Gains Tax (CGT) applies to the profit on any appreciating asset you dispose of. For Bitcoin holders, that means a percentage of your gain goes away before you see a cent.

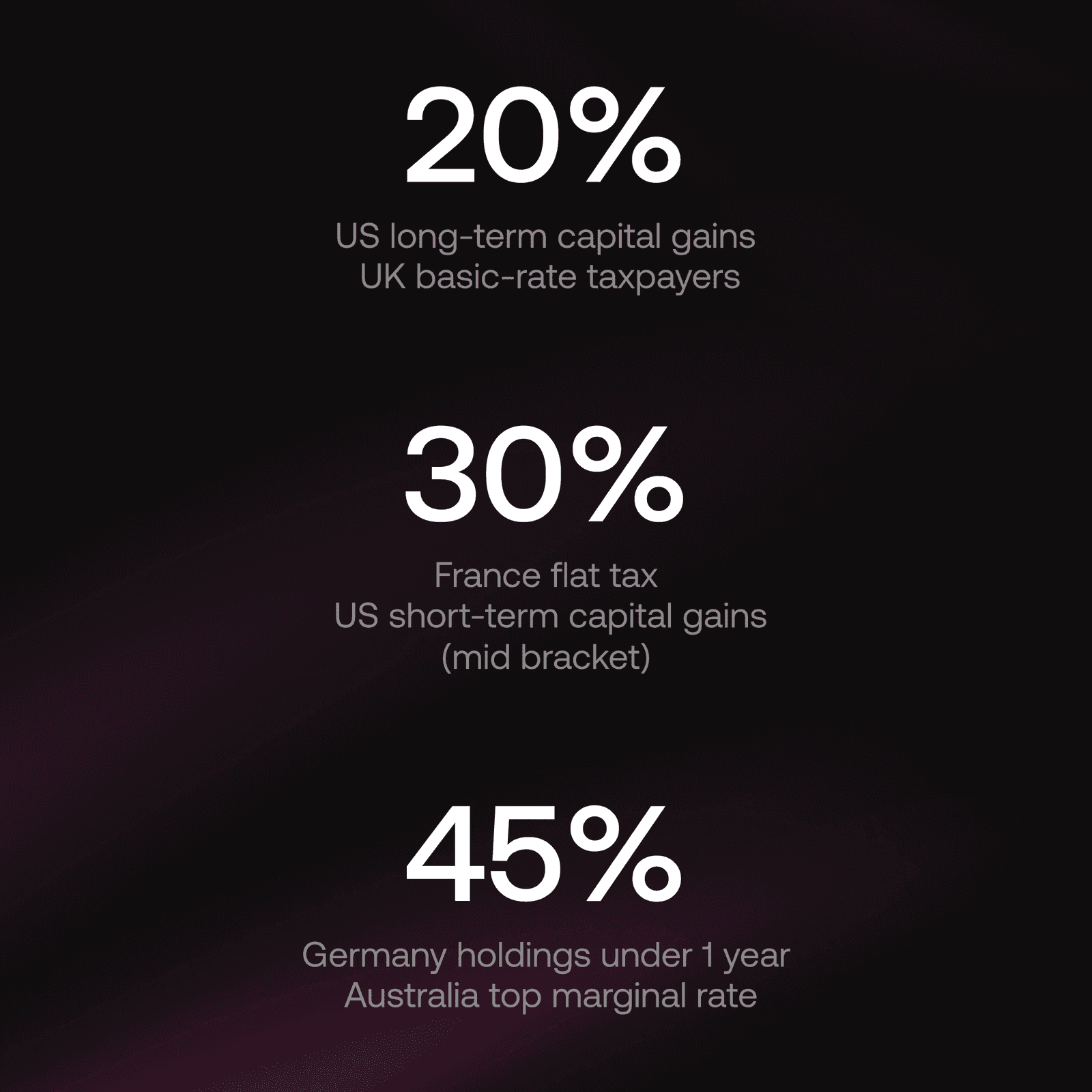

Rates vary significantly by country. US long-term holders pay 20%. French residents face a 30% flat rate. In Germany and Australia, top-rate taxpayers can face up to 45%.

Take a concrete example. You need $100,000 in liquidity. You hold BTC with an average cost basis of $10,000 per coin, and the current price is $71,000 (March 2024). To raise $100,000 by selling, you need to sell approximately 1.408 BTC. Each of those coins carries a taxable gain of $61,000, the difference between your $10,000 buy price and the $71,000 sale price.

At a 30% CGT rate, that comes to roughly $27,000 in tax just to access money that was already yours.

The second cost is less visible but larger. Once you sell those 1.408 BTC, they are gone. Every dollar of future appreciation on those coins belongs to someone else.

Chainflip's Bitcoin Lending Rate Is 3.13% APR vs. Up to 45% in Capital Gains Tax

Borrowing $100,000 against your BTC on Chainflip costs $3,130 in annual interest at 3.13% APR (as of March 3rd, 2026). That compares to $18,000 to $42,000 in tax depending on your jurisdiction.

To borrow $100,000, Chainflip's 80% maximum LTV requires $125,000 worth of BTC as collateral. At $71,000 per coin, that means locking 1.761 BTC. Those coins stay in the protocol, secured by Chainflip's validator set, and are returned when you repay the loan.

A loan is not a disposal. There is no CGT liability. The money reaches your wallet without a tax event, and your 1.761 BTC continues to appreciate throughout the loan term.

Scenario: bought BTC at $10,000 / current price $71,000 (Mar 2024) / accessing $100,000 in liquidity / 60% BTC appreciation assumed over 12 months:

Factor | Sell BTC: 20% CGT (US / UK) | Sell BTC: 30% CGT (France / US short-term) | Sell BTC: 45% CGT (Germany / Australia) | Borrow via Chainflip: 3.13% APR |

|---|---|---|---|---|

Taxable gain per BTC | $61,000 | $61,000 | $61,000 | None |

Tax event | Yes, 20% CGT | Yes, 30% CGT | Yes, 45% CGT | None |

Tax on gain | $17,183 | $25,775 | $38,662 | — |

Interest (3.13% APR) | — | — | — | $3,120 |

Net cash received | $82,817 | $74,225 | $61,338 | $96,880 |

BTC retained | None | None | None | 2.113 BTC |

1yr outcome | $82,817 | $74,225 | $61,338 | $236,880 |

How Chainflip's Native Bitcoin Lending Works

You deposit BTC as collateral and borrow USDC against it at a fixed loan-to-value ratio. Chainflip's maximum LTV at loan creation is 80%, meaning $100,000 borrowed requires $125,000 in BTC collateral.

At $71,000 per BTC, accessing $100,000 requires locking 1.761 BTC. You receive the USDC, your collateral stays in the protocol secured by validators, and when you repay the principal your BTC is returned in full.

The only cost is interest. At 3.13% APR on a $100,000 loan, that is $3,130 over twelve months.

Compare that to the sell scenario: you permanently part with 1.408 BTC, pay CGT on the gain, and receive less than $100,000 after tax. The loan requires more BTC locked as collateral, but you get all of it back.

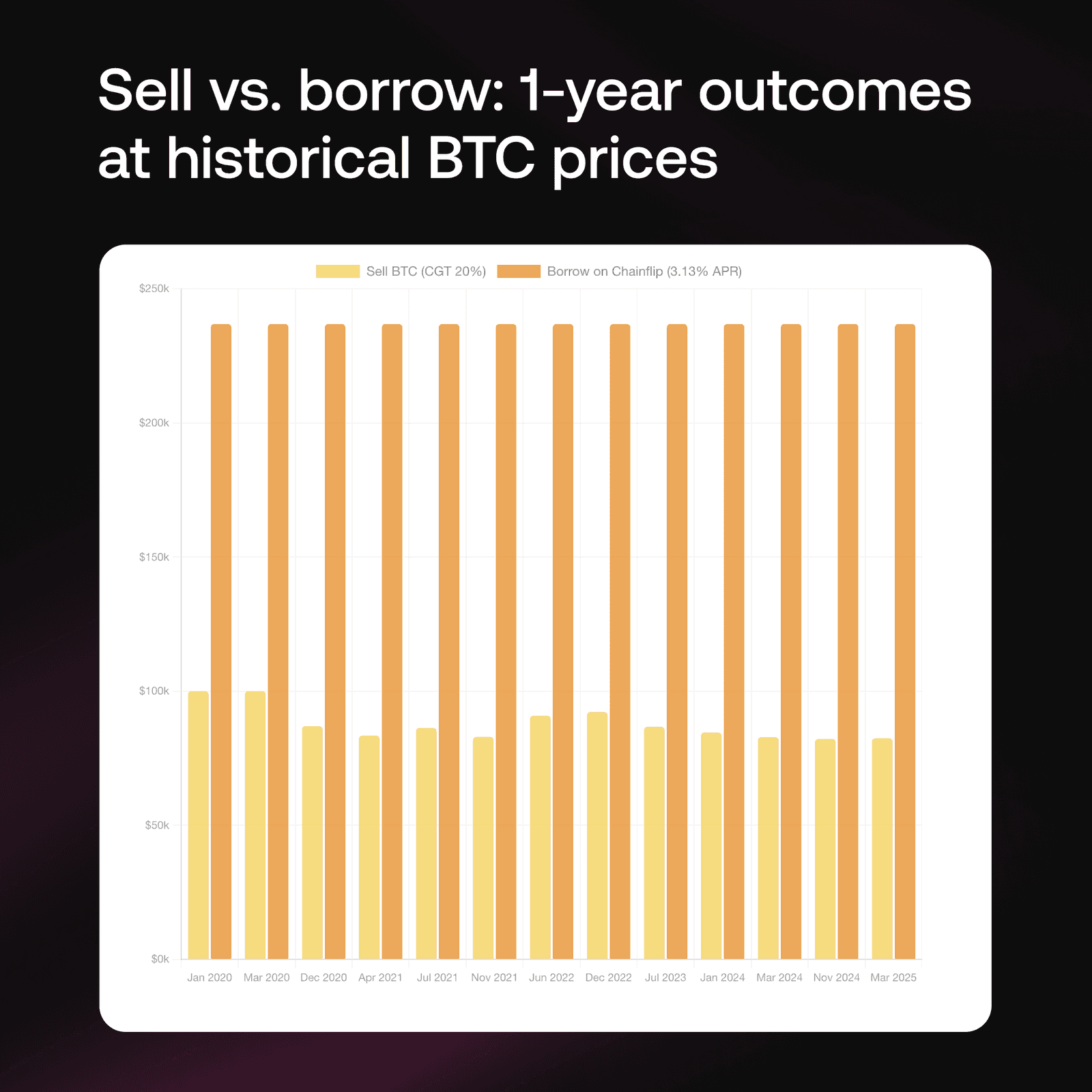

Borrowing Against BTC Outperforms Selling at Every Major Price Point Since 2020

The March 2024 example is not a cherry-picked scenario. Across every significant BTC price point since 2020, borrowing $100,000 produces a better 1-year outcome than raising $100,000 by selling.

At each price point, the sell scenario requires liquidating enough BTC to raise $100,000 and paying CGT on the gain above the $10,000 cost basis. The loan scenario locks 125% collateral at the same price and pays 3.13% interest. The chart shows 1-year projected outcomes for both, assuming 60% BTC appreciation and principal repaid at end of term.

The loan outcome consistently exceeds the sell outcome. The gap is largest at peak BTC prices, which is exactly when the pressure to sell tends to be highest.

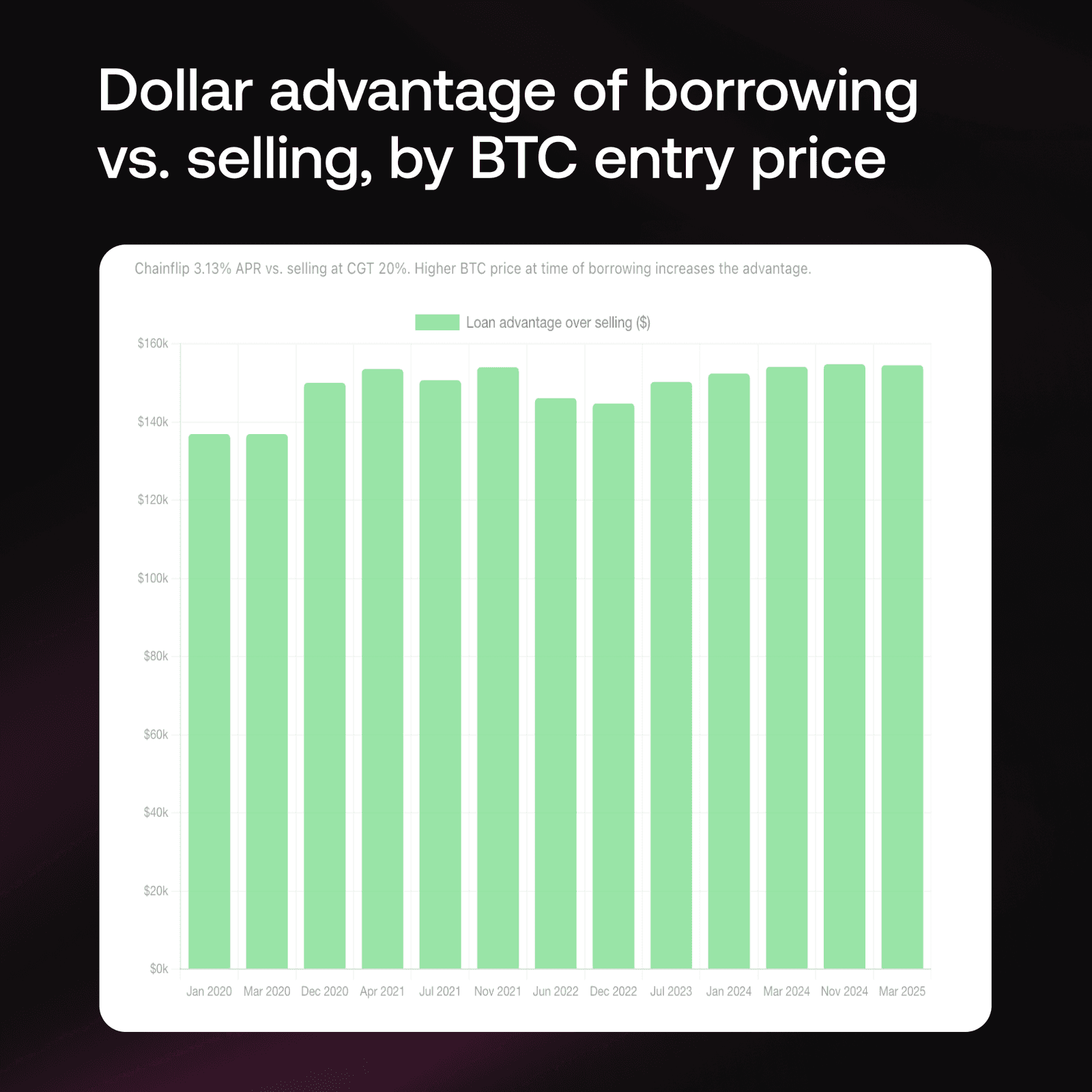

The Dollar Difference Between Selling and Borrowing Against BTC, Across Every Cycle

Here is the same data expressed as a single number: how many dollars better off you are by borrowing $100,000 instead of selling BTC to raise $100,000 at each historical price point.

Even at BTC's lower price points the advantage is material. At November 2021 prices ($69,000), the difference runs well into six figures. That is the cost of permanently liquidating part of your position before the next leg of a cycle.

The Higher Your CGT Rate, the More a Bitcoin-Backed Loan Saves You

The higher your local tax rate, the wider the gap between selling and borrowing becomes. The table below uses the same scenario throughout: need $100,000, bought BTC at $10,000 per coin, current price $71,000 (March 2024). The only variable is CGT rate.

Scenario: bought BTC at $10,000 / current price $71,000 (Mar 2024) / accessing $100,000 in liquidity / 60% BTC appreciation assumed over 12 months

Strategy | Rate | Cost to access $100k | Net cash received | BTC retained | 1yr outcome |

|---|---|---|---|---|---|

Sell BTC | 20% CGT US / UK | $17,183 in tax | $82,817 | None | $82,817 |

Sell BTC | 30% CGT France / US short-term | $25,775 in tax | $74,225 | None | $74,225 |

Sell BTC | 45% CGT Germany / Australia | $38,662 in tax | $61,338 | None | $61,338 |

Borrow on Chainflip | 3.13% APR | $3,120 in interest | $96,880 | Full (80% max LTV) | $236,880 |

Chainflip's borrow rate does not change based on your jurisdiction. Your tax bill does.

At 45% CGT, selling enough BTC to raise $100,000 costs $42,147 in tax alone. The Chainflip loan costs $3,130 in interest. That is a 13x difference in the cost of accessing the same liquidity, before accounting for the BTC upside forfeited by selling.

Selling BTC vs. Borrowing Against It on Chainflip: Full Comparison

Factor | Selling BTC | Borrowing on Chainflip |

|---|---|---|

Tax event | Yes. CGT on all gains above cost basis | No. A loan is not a disposal |

Cost to access $100k | $18k to $42k in tax | $3,130 in interest (3.13% APR) |

BTC upside retained | No. Position closed on sale | Yes. Collateral appreciates during loan |

Re-entry risk | High. Must repurchase at market price | None. Position was never closed |

Custody model | Centralized exchange required | Validator-custodied. No centralized intermediary |

Liquidation risk | None | Yes, if BTC falls below liquidation threshold |

Best suited for | Sellers needing certainty regardless of price | Long-term holders wanting liquidity without exiting |

One honest caveat: borrowing carries liquidation risk. If BTC drops significantly during the loan term, collateral can be liquidated to cover the position. Selling carries no such risk, and that tradeoff is worth factoring into your decision.

For long-term holders with conviction in BTC's direction, the risk profile of a loan is manageable. For someone who needs certainty regardless of price movement, selling may still be appropriate.

Why Chainflip's Bitcoin Lending Uses No Centralized Custodian

Chainflip's lending operates without a centralized custodian. Collateral is secured by Chainflip's validator set using a decentralized custody model, with no single point of control over deposited assets.

This differs from centralized lending platforms, where collateral is held by a company and subject to counterparty risk. Chainflip's crypto-economic security model means validator-custodied assets are governed by protocol rules, not company policy.

The current borrow rate is 3.13% APR (source: https://lp.chainflip.io/lending, March 3rd, 2026). Loans are denominated in USDC. Maximum LTV at loan creation is 80%.

Resources

Lend BTC - Borrow against Bitcoin

Swap Now - Start swapping native assets

Blog - Product updates and announcements

Chainflip Scan - Track swaps and network activity

Website - Explore Chainflip

Other Chainflip Products:

Boost - Earn fees by providing single-sided liquidity with no IL risk

Stablecoin Strategies - Deposit stablecoins and earn optimized yields

Provide Liquidity - Supply assets to Chainflip's liquidity pools

Stake FLIP - Delegate FLIP and earn staking rewards

Find us:

Discord - Join the Chainflip community

Telegram - Get the latest Chainflip updates

X - Follow Chainflip on X

LinkedIn - Chainflip on LinkedIn

YouTube - Chainflip tutorials and explainers

Threads - Follow Chainflip on Threads

Bluesky - Follow Chainflip on Bluesky

Frequently Asked Questions

What is the current Bitcoin lending rate on Chainflip? The current rate is 3.13% APR as of March 3rd, 2026. Rates may change based on protocol parameters. Check lp.chainflip.io/lending for the live rate.

Does borrowing against Bitcoin trigger capital gains tax? In most jurisdictions, taking out a loan against an asset is not a disposal and does not trigger CGT. Tax treatment varies by country. Consult a tax professional for advice specific to your situation.

How much BTC do I need to borrow $100,000 on Chainflip? At Chainflip's 80% maximum LTV, borrowing $100,000 requires $125,000 worth of BTC as collateral. At $71,000 per BTC that is 1.761 BTC. At $84,000 per BTC that is 1.488 BTC. The exact amount scales with the current price.

What is the maximum LTV on Chainflip's Bitcoin lending? The maximum LTV when opening a new loan is 80%. This means to borrow $100,000 in USDC, you need at least $125,000 worth of BTC as collateral. Soft liquidation begins if your LTV rises to 90%, and hard liquidation triggers at 95%.

What happens to my BTC collateral if the price drops? If your collateral value falls and your LTV rises above 90%, soft liquidation begins — the protocol sells small chunks of collateral to bring the loan back to a healthy ratio. Hard liquidation triggers at 95% LTV. Monitoring your LTV and adding collateral if BTC drops significantly reduces this risk.

Is there a centralized custodian holding collateral on Chainflip? No. Collateral is secured by Chainflip's validator set using a decentralized custody model. There are no centralized intermediaries with unilateral control over deposited assets.

Can I repay a Chainflip BTC-backed loan early? Yes. You can repay at any time and reclaim your collateral in full.

Assumptions: All examples based on raising $100,000 in liquidity. Sell scenario: sell enough BTC at the prevailing price to raise $100,000, pay CGT on the gain above $10,000 cost basis per coin. Loan scenario: lock 125% of loan value in BTC collateral at the prevailing price (80% max LTV), pay 3.13% APR interest, repay principal at end of term. BTC prices from historical market data. CGT rates modelled at 20% (US long-term / UK basic rate), 30% (France flat / US short-term mid bracket), 45% (Germany / Australia top marginal rate). 60% BTC price appreciation modelled over 12 months. Liquidation risk not modelled in outcome charts. For educational purposes only. Not financial or tax advice.

Selling BTC to access liquidity costs more than most people expect. The price on the screen is not what you receive. Capital Gains Tax (CGT) applies to the profit on any appreciating asset you dispose of. For Bitcoin holders, that means a percentage of your gain goes away before you see a cent.

Rates vary significantly by country. US long-term holders pay 20%. French residents face a 30% flat rate. In Germany and Australia, top-rate taxpayers can face up to 45%.

Take a concrete example. You need $100,000 in liquidity. You hold BTC with an average cost basis of $10,000 per coin, and the current price is $71,000 (March 2024). To raise $100,000 by selling, you need to sell approximately 1.408 BTC. Each of those coins carries a taxable gain of $61,000, the difference between your $10,000 buy price and the $71,000 sale price.

At a 30% CGT rate, that comes to roughly $27,000 in tax just to access money that was already yours.

The second cost is less visible but larger. Once you sell those 1.408 BTC, they are gone. Every dollar of future appreciation on those coins belongs to someone else.

Chainflip's Bitcoin Lending Rate Is 3.13% APR vs. Up to 45% in Capital Gains Tax

Borrowing $100,000 against your BTC on Chainflip costs $3,130 in annual interest at 3.13% APR (as of March 3rd, 2026). That compares to $18,000 to $42,000 in tax depending on your jurisdiction.

To borrow $100,000, Chainflip's 80% maximum LTV requires $125,000 worth of BTC as collateral. At $71,000 per coin, that means locking 1.761 BTC. Those coins stay in the protocol, secured by Chainflip's validator set, and are returned when you repay the loan.

A loan is not a disposal. There is no CGT liability. The money reaches your wallet without a tax event, and your 1.761 BTC continues to appreciate throughout the loan term.

Scenario: bought BTC at $10,000 / current price $71,000 (Mar 2024) / accessing $100,000 in liquidity / 60% BTC appreciation assumed over 12 months:

Factor | Sell BTC: 20% CGT (US / UK) | Sell BTC: 30% CGT (France / US short-term) | Sell BTC: 45% CGT (Germany / Australia) | Borrow via Chainflip: 3.13% APR |

|---|---|---|---|---|

Taxable gain per BTC | $61,000 | $61,000 | $61,000 | None |

Tax event | Yes, 20% CGT | Yes, 30% CGT | Yes, 45% CGT | None |

Tax on gain | $17,183 | $25,775 | $38,662 | — |

Interest (3.13% APR) | — | — | — | $3,120 |

Net cash received | $82,817 | $74,225 | $61,338 | $96,880 |

BTC retained | None | None | None | 2.113 BTC |

1yr outcome | $82,817 | $74,225 | $61,338 | $236,880 |

How Chainflip's Native Bitcoin Lending Works

You deposit BTC as collateral and borrow USDC against it at a fixed loan-to-value ratio. Chainflip's maximum LTV at loan creation is 80%, meaning $100,000 borrowed requires $125,000 in BTC collateral.

At $71,000 per BTC, accessing $100,000 requires locking 1.761 BTC. You receive the USDC, your collateral stays in the protocol secured by validators, and when you repay the principal your BTC is returned in full.

The only cost is interest. At 3.13% APR on a $100,000 loan, that is $3,130 over twelve months.

Compare that to the sell scenario: you permanently part with 1.408 BTC, pay CGT on the gain, and receive less than $100,000 after tax. The loan requires more BTC locked as collateral, but you get all of it back.

Borrowing Against BTC Outperforms Selling at Every Major Price Point Since 2020

The March 2024 example is not a cherry-picked scenario. Across every significant BTC price point since 2020, borrowing $100,000 produces a better 1-year outcome than raising $100,000 by selling.

At each price point, the sell scenario requires liquidating enough BTC to raise $100,000 and paying CGT on the gain above the $10,000 cost basis. The loan scenario locks 125% collateral at the same price and pays 3.13% interest. The chart shows 1-year projected outcomes for both, assuming 60% BTC appreciation and principal repaid at end of term.

The loan outcome consistently exceeds the sell outcome. The gap is largest at peak BTC prices, which is exactly when the pressure to sell tends to be highest.

The Dollar Difference Between Selling and Borrowing Against BTC, Across Every Cycle

Here is the same data expressed as a single number: how many dollars better off you are by borrowing $100,000 instead of selling BTC to raise $100,000 at each historical price point.

Even at BTC's lower price points the advantage is material. At November 2021 prices ($69,000), the difference runs well into six figures. That is the cost of permanently liquidating part of your position before the next leg of a cycle.

The Higher Your CGT Rate, the More a Bitcoin-Backed Loan Saves You

The higher your local tax rate, the wider the gap between selling and borrowing becomes. The table below uses the same scenario throughout: need $100,000, bought BTC at $10,000 per coin, current price $71,000 (March 2024). The only variable is CGT rate.

Scenario: bought BTC at $10,000 / current price $71,000 (Mar 2024) / accessing $100,000 in liquidity / 60% BTC appreciation assumed over 12 months

Strategy | Rate | Cost to access $100k | Net cash received | BTC retained | 1yr outcome |

|---|---|---|---|---|---|

Sell BTC | 20% CGT US / UK | $17,183 in tax | $82,817 | None | $82,817 |

Sell BTC | 30% CGT France / US short-term | $25,775 in tax | $74,225 | None | $74,225 |

Sell BTC | 45% CGT Germany / Australia | $38,662 in tax | $61,338 | None | $61,338 |

Borrow on Chainflip | 3.13% APR | $3,120 in interest | $96,880 | Full (80% max LTV) | $236,880 |

Chainflip's borrow rate does not change based on your jurisdiction. Your tax bill does.

At 45% CGT, selling enough BTC to raise $100,000 costs $42,147 in tax alone. The Chainflip loan costs $3,130 in interest. That is a 13x difference in the cost of accessing the same liquidity, before accounting for the BTC upside forfeited by selling.

Selling BTC vs. Borrowing Against It on Chainflip: Full Comparison

Factor | Selling BTC | Borrowing on Chainflip |

|---|---|---|

Tax event | Yes. CGT on all gains above cost basis | No. A loan is not a disposal |

Cost to access $100k | $18k to $42k in tax | $3,130 in interest (3.13% APR) |

BTC upside retained | No. Position closed on sale | Yes. Collateral appreciates during loan |

Re-entry risk | High. Must repurchase at market price | None. Position was never closed |

Custody model | Centralized exchange required | Validator-custodied. No centralized intermediary |

Liquidation risk | None | Yes, if BTC falls below liquidation threshold |

Best suited for | Sellers needing certainty regardless of price | Long-term holders wanting liquidity without exiting |

One honest caveat: borrowing carries liquidation risk. If BTC drops significantly during the loan term, collateral can be liquidated to cover the position. Selling carries no such risk, and that tradeoff is worth factoring into your decision.

For long-term holders with conviction in BTC's direction, the risk profile of a loan is manageable. For someone who needs certainty regardless of price movement, selling may still be appropriate.

Why Chainflip's Bitcoin Lending Uses No Centralized Custodian

Chainflip's lending operates without a centralized custodian. Collateral is secured by Chainflip's validator set using a decentralized custody model, with no single point of control over deposited assets.

This differs from centralized lending platforms, where collateral is held by a company and subject to counterparty risk. Chainflip's crypto-economic security model means validator-custodied assets are governed by protocol rules, not company policy.

The current borrow rate is 3.13% APR (source: https://lp.chainflip.io/lending, March 3rd, 2026). Loans are denominated in USDC. Maximum LTV at loan creation is 80%.

Resources

Lend BTC - Borrow against Bitcoin

Swap Now - Start swapping native assets

Blog - Product updates and announcements

Chainflip Scan - Track swaps and network activity

Website - Explore Chainflip

Other Chainflip Products:

Boost - Earn fees by providing single-sided liquidity with no IL risk

Stablecoin Strategies - Deposit stablecoins and earn optimized yields

Provide Liquidity - Supply assets to Chainflip's liquidity pools

Stake FLIP - Delegate FLIP and earn staking rewards

Find us:

Discord - Join the Chainflip community

Telegram - Get the latest Chainflip updates

X - Follow Chainflip on X

LinkedIn - Chainflip on LinkedIn

YouTube - Chainflip tutorials and explainers

Threads - Follow Chainflip on Threads

Bluesky - Follow Chainflip on Bluesky

Frequently Asked Questions

What is the current Bitcoin lending rate on Chainflip? The current rate is 3.13% APR as of March 3rd, 2026. Rates may change based on protocol parameters. Check lp.chainflip.io/lending for the live rate.

Does borrowing against Bitcoin trigger capital gains tax? In most jurisdictions, taking out a loan against an asset is not a disposal and does not trigger CGT. Tax treatment varies by country. Consult a tax professional for advice specific to your situation.

How much BTC do I need to borrow $100,000 on Chainflip? At Chainflip's 80% maximum LTV, borrowing $100,000 requires $125,000 worth of BTC as collateral. At $71,000 per BTC that is 1.761 BTC. At $84,000 per BTC that is 1.488 BTC. The exact amount scales with the current price.

What is the maximum LTV on Chainflip's Bitcoin lending? The maximum LTV when opening a new loan is 80%. This means to borrow $100,000 in USDC, you need at least $125,000 worth of BTC as collateral. Soft liquidation begins if your LTV rises to 90%, and hard liquidation triggers at 95%.

What happens to my BTC collateral if the price drops? If your collateral value falls and your LTV rises above 90%, soft liquidation begins — the protocol sells small chunks of collateral to bring the loan back to a healthy ratio. Hard liquidation triggers at 95% LTV. Monitoring your LTV and adding collateral if BTC drops significantly reduces this risk.

Is there a centralized custodian holding collateral on Chainflip? No. Collateral is secured by Chainflip's validator set using a decentralized custody model. There are no centralized intermediaries with unilateral control over deposited assets.

Can I repay a Chainflip BTC-backed loan early? Yes. You can repay at any time and reclaim your collateral in full.

Assumptions: All examples based on raising $100,000 in liquidity. Sell scenario: sell enough BTC at the prevailing price to raise $100,000, pay CGT on the gain above $10,000 cost basis per coin. Loan scenario: lock 125% of loan value in BTC collateral at the prevailing price (80% max LTV), pay 3.13% APR interest, repay principal at end of term. BTC prices from historical market data. CGT rates modelled at 20% (US long-term / UK basic rate), 30% (France flat / US short-term mid bracket), 45% (Germany / Australia top marginal rate). 60% BTC price appreciation modelled over 12 months. Liquidation risk not modelled in outcome charts. For educational purposes only. Not financial or tax advice.

Integrations

Announcements

Swap

MakePay Adds Cross-Chain Payments to BTCPay Server With Chainflip

MakePay Adds Cross-Chain Payments to BTCPay Server With Chainflip

Swap

How-to

Integrations

How to Swap Native TRX and USDT-TRC20 Using MetaMask via Chainflip

How to Swap Native TRX and USDT-TRC20 Using MetaMask via Chainflip